October 31, 2023 12 mins

5 Ways Artificial Intelligence can Boost Claims Management

(Re)insurers must embrace AI technology to successfully navigate today’s emerging transformative trends that are shaping the insurance landscape.

Key Takeaways

-

The insurance industry is looking for ways to attract people with the right mindset and skills for a fast-changing business environment.

-

Diverse skills and viewpoints are vital to inform business strategy, while future underwriting teams should be more collaborative, blending technical and people skills.

-

Leadership is key to successfully manage talent transformation and create an open, respectful and inclusive culture.

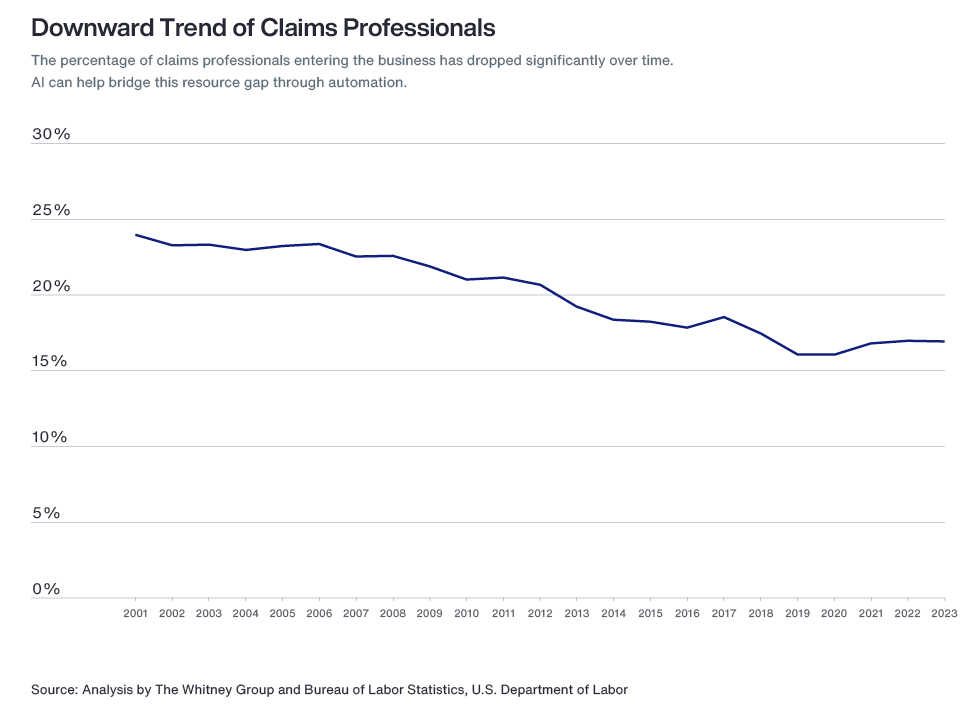

An aging population, reliance on AI, and new technological, environmental, financial and social risks, are top of mind issues for many claims leaders. An aging claims workforce, coupled with growing loss costs and expenses, have resulted in record high combined ratios. This presents insurers with a unique dilemma: how to ensure proper claims outcomes and lower claims spend, with an increasingly less experienced and knowledgeable talent pool.

Adopting available artificial intelligence (AI) today and preparing for future iterations, is critical for (re)insurers to address emerging transformative trends that shape our industry proactively and with the greatest impact possible. In fact, developing a comprehensive claims AI strategy, which reimagines an organization’s plan for people, process, technology and risk, is critical to achieve some of the estimated $100 billion in gross written premium, as well as associated expense savings.

Current Drivers of Claims Quality

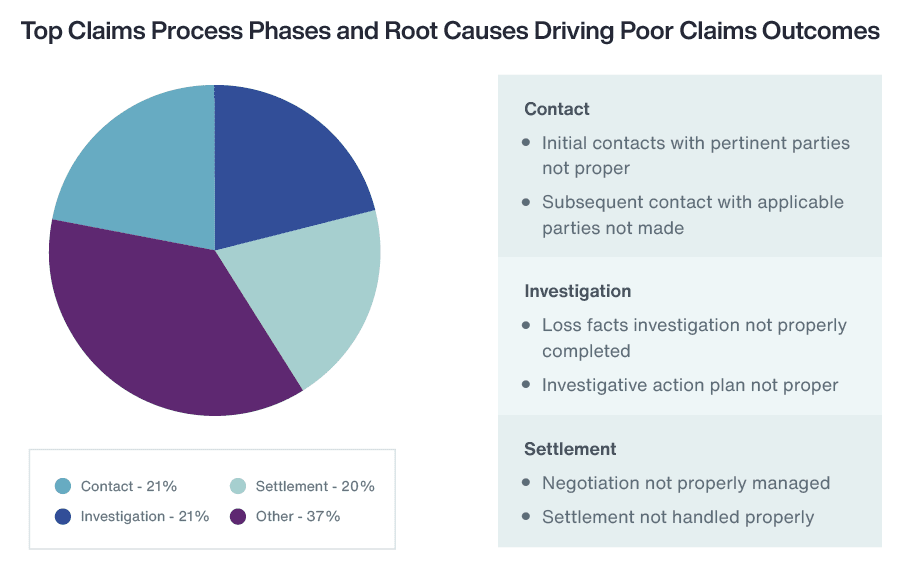

To better understand where and how to infuse AI in the claims process, take a step back and look at the current drivers of claims quality. Aon’s Strategy and Technology Group (STG) benchmarked over 100 claims operations and found the greatest opportunity to drive claims quality improvement reside in the phases of contact, investigation and settlement.

Much of the work involved in managing these areas of the claims process requires extensive human resources, in addition to manual, often repetitive tasks that are prone to duplication and error. Embracing AI will also help close the retirement and skill gaps due to an ageing insurance workforce combined with less skilled claims handlers involved in the claims process.

Source: Analysis by The Whitney Group and Bureau of Labor Statistics, US Department of Labor

Organizations that invest in claims AI solutions today can begin to soften the blow of impending retirements, while giving new claims talent the time and support to learn, grow and develop the expertise left behind by retirees.

It is important to understand the potential for AI capabilities to expand its focus from data capture, sorting, summarizing and analyzing, to an emphasis on prescribing recommended go-forward actions. It will allow (re)insurers to anticipate the challenges to come with emerging risks and plan for the best way to maintain and/or increase process efficiency and improve customer satisfaction.

Examples of AI use in claims include optical character recognition to review documents when investigating claims, applying predictive analytics to identify fraud, or the development of prescriptive analytics to automate end-to-end claims processing.

How AI Helps Claims Now and in the Future

Strategic use of AI can optimize claims processes — from claim intake through claim payment — and yield efficiency and productivity benefits. Examples of these include:

-

1. First Notice of Loss (FNOL)

At FNOL, IOT/telematics capabilities can be implemented to alert insurers via smart phones, home assistants or smart cars when a potential property or auto claim has occurred. The use of chat boxes aims to alleviate the need for allocating resources to perform repeated administrative tasks and facilitate the reporting and initial information gathering process. Communication with claimants and insureds alike becomes more streamlined and convenient through the adoption of mobile apps and texting features.

-

2. Investigation and Coverage Determination

When it comes to investigating claims and determining coverage, AI adoption is expected to increase productivity, which can result in reduced cycle times. Optical character recognition can auto-interpret and categorize handwritten documents that are common in police and medical reports, allowing the claims handler to dedicate their time to evaluating damages, liability and coverage. Similarly, computer vision and using devices like intelligent drones to interpret images and videos, optimizes the investigation process by systematically creating damage estimates. Fraud is more quickly and effectively detected through use of advanced analytics, information correlation and predictions.

-

3. Valuation and Payment

Determining a claim’s value and issuing payment is supported via distributed ledger AI. This records transaction data in real-time and automates processes when specific circumstances occur to predict a value, thereby creating automatic estimates. It is also effective in aligning events and behaviors based on payment preferences and subrogation processes. Similarly, chatbots and texting solutions can help make payment arrangements, while advanced analytics correlates policy checks and payment calculations.

Futureproofing Your Organization

With AI now ever more integral to claims processes, it’s often overwhelming to determine when, where and how to best implement it. Developing a comprehensive strategic AI plan that considers people (customer preferences and internal talent readiness), processes, technology and risk is fundamental to effective AI integration. Use these steps as a guide:

Respond to customer preferences

Customer preferences regarding human to AI engagement are shaped by factors such as claim type, claim severity/complexity and demographics. For that reason, it is imperative that insurers develop a full understanding of the types of customers they service and the types of claims they manage.

Commercial customers who deal with higher claim frequency are familiar with claims processes, and tend to have limited emotional ties to their claims. These customers could reasonably prefer a more digital and automated claims experience. Personal customers, on the other hand, when dealing with bodily injury, litigation or extensive damage, may better appreciate being serviced more directly by a claims professional to help set expectations, provide a degree of emotional support and answer questions unique to their claim. Age, geographic location and degree of education may also play a part. Considering these factors will help insurers develop an AI strategy that correlates best to their customers’ needs.

Identify talent readiness

An effective assessment of people also includes an examination of talent readiness for AI adoption. Identifying skills gaps, evaluating current and future staffing demands and adapting to the changing market are imperative. AI is not expected to remove people entirely from the equation, but rather enhance and improve processes allowing for human resource reallocation to more productive and meaningful work. While AI will allow employees to refocus on more substantive and analytical work, it also requires skills to effectively monitor and track AI functionality and use.

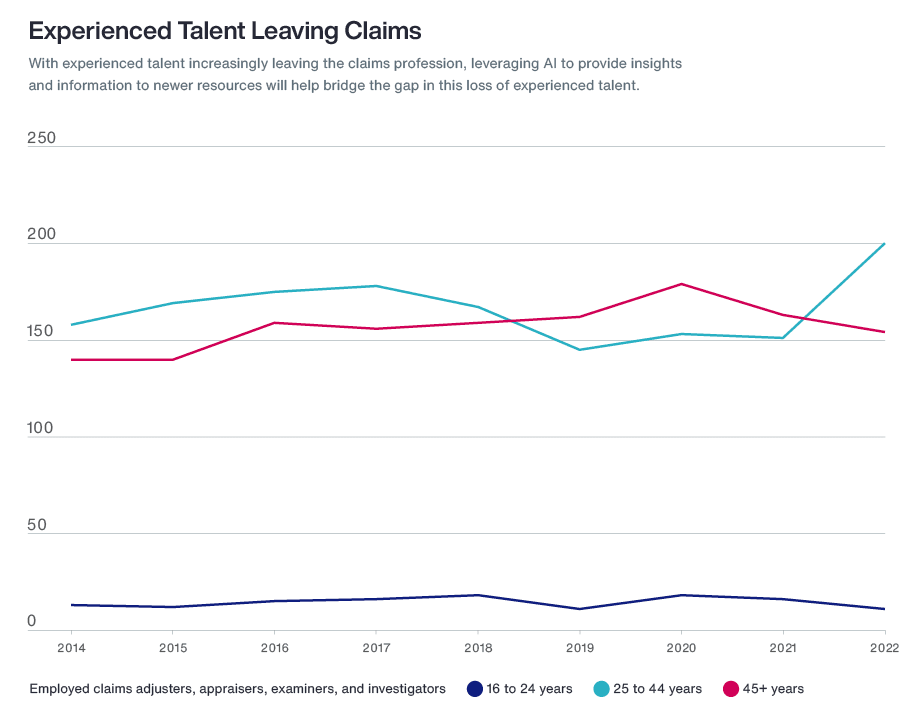

When determining what type and where in the claims process AI may be most impactful, assessing a claims professional’s current and long-term experience levels cannot be overlooked. With many retiring, (re)insurers must look for ways to replace or otherwise support their organizations to minimize the impact of not just losing claims handlers, but also the coaches and mentors that support their less experienced staff. AI can potentially provide those who are less experienced with comprehensive training and the opportunity to work more directly with supervisors and managers, while also spending extra time on the most meaningful phases of claims management.

Change can be challenging. Understanding the questions and concerns of your AI strategy and getting ahead of colleague pushback with transparent, meaningful and ongoing communication is key.

(Re)insurers must first be clear on their strategic direction and growth plans before they get into scaling talent activity. Otherwise, it’s like preparing for a journey without knowing the destination, often resulting in wasted time and effort.

Map processes

In addition to a full understanding of potential people challenges, establishing a detailed workflow for all areas of claims processes is foundational to AI success. It is not enough to identify the high-level steps of managing a claim. Developing a workflow map of end-to-end processes for each line of business and all claims functions that capture time spent and resources allocated, brings to light gaps and opportunities for greater efficiency, productivity and improved quality.

AI support should focus on the following areas:

- Repetitive tasks

- Time consuming work

- Tasks involving multiple resources, systems and/or tools

- Inconsistently performed tasks that could benefit from standardization

Once gaps and opportunities are identified, the next step is determining how to incorporate AI into the process. Insurers could either partner with an AI vendor, acquire AI technology, or build the technology within their organization.

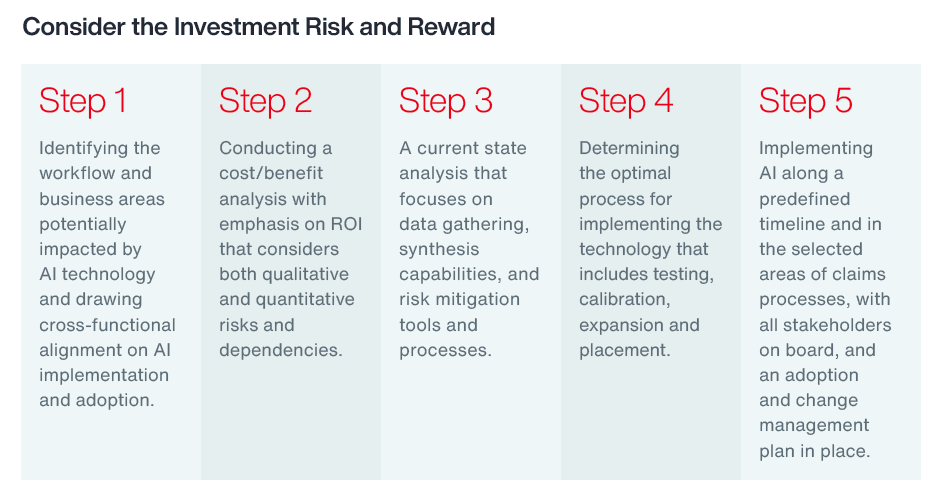

Consider the investment risk and reward

AI implementation should be balance sheet tolerant. The optimal method for AI implementation considers cost, a current state analysis and plans for AI to fully meet anticipated expectations.

Understand the risks of AI

Technological risks are those inherent to the AI solution and independent of human interaction. Because AI collects, stores and processes personal data, data privacy leaks can occur creating data confidentiality risks. AI may also be vulnerable to security risks. Algorithms are the parameters that train AI to develop insights. If an algorithm is leaked, the model can be copied, therefore compromising data. Finally, most AI solutions currently do not effectively track how it makes decisions. This lack of transparency makes it difficult to fix systems when unwanted outcomes occur. This can be problematic in the highly regulated insurance arena, especially when responding to inquiries or audits.

Usage risks are those that result from human interference. AI depends on the learned or trained data. Incorrect or biased data will produce inaccurate or distorted results. Additionally, there is potential for incorrect AI output. Users often lack awareness of what AI is, what it does and how it performs. Finally, AI could be used for a purpose outside of original intent, and thus compromised, causing adverse outcomes.

Although AI risks can be significant, implementing structured governance will help mitigate these threats. Effective governance consists of:

- Tracking all business objectives;

- Determining if the objectives are being met;

- Assessing whether modifications are needed; and

- Implementing and testing any modification.

The strength and reliability of AI governance impacts ROI analysis and ultimately an insurer’s appetite to integrate AI into its claims processes.

Use Cases

As AI technology solutions evolve and grow, (re)insurers have various options to optimize the key claims quality drivers of contact, investigation, and settlement with AI, and to evolve their claims quality programs. In this section we delve into case studies detailing some of these options.

Next Steps to Boost Claims Management with AI

AI possess the power to not only transform the claims process, but also fill the skills gap due to an aging claims professional population and lack of new resources. The most successful insurers will be the ones who take the time now to create a strategic AI plan for the future. Insurers that have a full understanding of their people, process, technologies and risks associated with implementing this new technology will gain a competitive advantage over competitors. They will become more efficient, improve customer service and achieve better claims outcomes to significantly lower loss ratios and ensure future financial success.

Glossary:

What is AI?

With all the latest talk about AI, most claims professionals do not really know what it is or how it can be applied to claims functions. AI was created in the ‘60s and ‘70s and refers to mathematical models that learn patterns from data and enable faster or even automated decisions. As a machine-based system, AI can, for a given set of human-defined objectives, make predictions, recommendations and decisions that influence real and virtual environments. Although various categorizations of AI exist, AI can most simply be bucketed into two categories today: traditional and generative.

Traditional AI

Traditional AI relies on predefined rules and patterns to perform specific tasks. It has been largely restricted to an approach based on use cases, optimizing niches of existing operating models rather than fundamentally transforming them. It is designed to fulfil a specific purpose in a defined context, and strong reliance exists on labeled data for training, as well as human-crafted features. Put another way, traditional AI is often limited to the quality and quantity of the labeled data available during training. Examples include: automated insights, predictive modelling, intelligent alerting or platforms like Google, YouTube, Netflix or Amazon.

Generative AI

Generative AI operates through deep learning models and advanced algorithms, often without the need for highly structured data input. It can be a catalyst for transforming, redesigning end-to-end operating models by creating new content based on past inputs. Because generative AI is not strictly bound by fixed rules, it can create original and dynamic outputs without direct supervision. It learns from both labeled and unstructured data and can produce meaningful outputs that go beyond the training data, to the point of even summarizing large amounts of unstructured data (such as web or document content). Today, we can see this in Google Bard or ChatGPT. Future iterations of generative AI are expected to include prescriptive technology that not only predicts outcomes, but also suggests the actions to be taken based on the data it analyzes.

Proven use cases of traditional AI have already been adopted by many (re)insurers, while generative AI is just starting to take its foot hold with limited application within the claims process.

Discover More: Read more about our claims and client services for insurers, or contact our Strategy and Technology Group’s Claims team to learn how you can futureproof and boost your claims management processes.

General Disclaimer

This document is not intended to address any specific situation or to provide legal, regulatory, financial, or other advice. While care has been taken in the production of this document, Aon does not warrant, represent or guarantee the accuracy, adequacy, completeness or fitness for any purpose of the document or any part of it and can accept no liability for any loss incurred in any way by any person who may rely on it. Any recipient shall be responsible for the use to which it puts this document. This document has been compiled using information available to us up to its date of publication and is subject to any qualifications made in the document.

Terms of Use

The contents herein may not be reproduced, reused, reprinted or redistributed without the expressed written consent of Aon, unless otherwise authorized by Aon. To use information contained herein, please write to our team.

Aon's Better Being Podcast

Our Better Being podcast series, hosted by Aon Chief Wellbeing Officer Rachel Fellowes, explores wellbeing strategies and resilience. This season we cover human sustainability, kindness in the workplace, how to measure wellbeing, managing grief and more.

-

Podcast 23 mins

Better Being Series: Understanding Burnout in the Workplace -

Podcast 14 mins

Better Being Series: Why Nutrition Matters -

Podcast 10 mins

Better Being Series: Discover the ‘Blue Zones’ Where People Live Longer -

Podcast 20 mins

Better Being Series: Improving Your Financial Wellbeing -

Podcast 17 mins

Better Being Series: Are You Taking Care of Your Digital Wellbeing? -

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health -

Podcast 29 mins

On Aon’s Better Being Series: The World Wellbeing Movement -

Podcast 28 mins

On Aon’s Better Being Series: Mental Health and Creating Kinder Cultures -

Podcast 25 mins

On Aon’s Better Being Series: Managing Loss and Grief -

Podcast 24 mins

On Aon’s Better Being Series: Measuring Wellbeing -

Podcast 25 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience -

Podcast 23 mins

On Aon’s Better Being Series: Human Sustainability

Aon Insights Series Asia

Expert Views on Today's Risk Capital and Human Capital Issues

-

Article 8 mins

Thriving in an interconnected world: How the C-Suite embraces uncertainty -

Article 6 mins

Powering progress: Collaborating to build a sustainable future in emerging markets -

Article 5 mins

Building Business Resilience: Key Steps to Effectively Integrate Risk Management Across Your Organisation -

Article 7 mins

Why humans are the essential factor in the success of Artificial Intelligence (AI) -

Article 4 mins

Leveraging Research and Expertise to Strengthen Your HR Strategy for 2025 and Beyond

Aon Insights Series Pacific

Expert Views on Today's Risk Capital and Human Capital Issues

-

Article 5 mins

How Four Megatrends are Driving Strategic Business Priorities Around the World -

Article 2 mins

Unlocking New Solutions: The Rise of Parametric Insurance -

Article 3 mins

The Case for a National Workers’ Compensation Scheme

Aon Insights Series UK

Expert Views on Today's Risk Capital and Human Capital Issues

-

Article 2 mins

Introduction: Clarity and Confidence to Make Better Decisions -

Article 2 mins

The Age of Rising Resilience – An Economic Outlook -

Article 3 mins

Building Resilience Against the Constant Cyber Threat -

Article 2 mins

Making Better Decisions – A Treasurer’s Perspective -

Article 2 mins

How to Balance the Conflicting Forces of Efficiency, Performance and Wellbeing -

Article 3 mins

Seizing the Opportunity: Building a Comprehensive Approach to Risk Transfer -

Article 2 mins

Tapping New Markets to Unlock Deal Value -

Article 5 mins

The Rise of the Skills-Based Organisation -

Article 2 mins

Creating a Fair and Equitable Workforce for Everyone -

Article 3 mins

The Year of the Vote: How Geopolitical Volatility Will Impact Businesses -

Article 2 mins

The Aon Difference

Construction and Infrastructure

The construction industry is under pressure from interconnected risks and notable macroeconomic developments. Learn how your organization can benefit from construction insurance and risk management.

-

Article 8 mins

How North American Construction Contractors Can Mitigate Emerging Risks -

Article 7 mins

Managing Construction Risks: 7 Risk Advisory Steps -

Article 7 mins

Unlocking Capacity and Capital in a Challenging Construction Risk Market -

Article 7 mins

Protecting North American Contractors from Extreme Heat Risks with Parametric -

Article 5 mins

How Climate Modeling Can Mitigate Risks and Improve Resilience in the Construction Industry -

Report 1 mins

Construction Risk Management Europe Report 2023 -

Article 8 mins

Parametric Can Help Mitigate Extreme Heat Risks for Contractors in EMEA -

Article 9 mins

How the Construction Industry is Navigating Climate Change -

Article 11 mins

Top Risks Facing Construction and Real Estate Organizations

Cyber Labs

Stay in the loop on today's most pressing cyber security matters.

-

Cyber Labs 6 mins

Optimizing Your Cyber Resilience Strategy Through CISO and CRO Connectivity -

Cyber Labs 9 mins

Bypassing EDR through Retrosigned Drivers and System Time Manipulation -

Cyber Labs 10 mins

DNSForge – Responding with Force -

Cyber Labs 7 mins

Unveiling "sedexp": A Stealthy Linux Malware Exploiting udev Rules -

Cyber Labs 3 mins

Command Injection and Path Traversal in StoneFly Storage Concentrator -

Cyber Labs 7 mins

Adopt an AI Approach with Confidence, for CISOs and CIOs -

Cyber Labs 3 mins

Responding to the CrowdStrike Outage: Implications for Cyber and Technology Professionals -

Cyber Labs 10 mins

DUALITY Part II - Initial Access and Tradecraft Improvements -

Cyber Labs 17 mins

Cracking Into Password Requirements -

Cyber Labs 57 mins

DUALITY: Advanced Red Team Persistence through Self-Reinfecting DLL Backdoors for Unyielding Control -

Cyber Labs 7 mins

Restricted Admin Mode – Circumventing MFA On RDP Logons -

Cyber Labs 9 mins

Detecting “Effluence”, An Unauthenticated Confluence Web Shell -

Cyber Labs 10 mins

Flash Loan Attacks: A Case Study -

Cyber Labs 7 mins

Financially Motivated Criminal Group Targets Telecom, Technology & Manufacturing -

Cyber Labs 16 mins

New Burp Suite Extension: BlazorTrafficProcessor -

Cyber Labs 3 mins

Command Injection and Buffer Overflow in Multiple Sharp NEC Displays -

Cyber Labs 3 mins

Command Injection in Multiple Snap One Araknis Networks Products -

Cyber Labs 10 mins

CVE-2021-1825: Inadequate Input Encoding in WebKit -

Cyber Labs 3 mins

Unauthenticated XXE in Multiple Mitsubishi Electric Air Conditioner Control Systems -

Cyber Labs 12 mins

Finding more IDORs – Tips and Tricks

Cyber Resilience

Our Cyber Resilience collection gives you access to Aon’s latest insights on the evolving landscape of cyber threats and risk mitigation measures. Reach out to our experts to discuss how to make the right decisions to strengthen your organization’s cyber resilience.

-

Article 9 mins

Building Resilience in a Buyer-Friendly Cyber and E&O Market -

Article 11 mins

A Middle Market Roadmap for Cyber Resilience -

Article 8 mins

Lessons Learned from the CrowdStrike Outage: 5 Strategies to Build Cyber Resilience -

Article 8 mins

Responding to Cyber Attacks: How Directors and Officers and Cyber Policies Differ -

Article 7 mins

Why Now is the Right Time to Customize Cyber and E&O Contracts -

Article 6 mins

8 Steps Toward Building Better Resilience Against Rising Ransomware Attacks -

Article 7 mins

Mitigating Insider Threats: Managing Cyber Perils While Traveling Globally -

Article 5 mins

Managing Cyber Risk through Return on Security Investment -

Article 10 mins

Mitigating Insider Threats: Your Worst Cyber Threats Could be Coming from Inside -

Article 9 mins

Why HR Leaders Must Help Drive Cyber Security Agenda -

Article 10 mins

Escalating Cyber Security Risks Mean Businesses Need to Build Resilience

Employee Wellbeing

Our Employee Wellbeing collection gives you access to the latest insights from Aon's human capital team. You can also reach out to the team at any time for assistance with your employee wellbeing needs.

-

Article 9 mins

The Next Evolution of Wellbeing is About Performance -

Article 6 mins

Three Ways Collective Retirement Plans Support HR Priorities -

Article 9 mins

How the Right Employee Wellbeing Strategy Impacts Microstress and Burnout at Work -

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health -

Article 7 mins

Making Wellbeing Part of a Company’s DNA -

Podcast 24 mins

On Aon’s Better Being Series: Measuring Wellbeing -

Podcast 25 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience -

Article 7 mins

Why Workforce Wellbeing is Vital to Company Performance -

Article 7 mins

COVID-19 has Permanently Changed the Way We Think About Wellbeing

Environmental, Social and Governance Insights

Explore Aon's latest environmental social and governance (ESG) insights.

-

Article 8 mins

Why ESG Is Even More Important In A Crisis Like COVID-19 -

Podcast 16 mins

On Aon Podcast: Approach to DE&I in the Workplace

Q4 2023 Global Insurance Market Insights

Our Global Insurance Market Insights highlight insurance market trends across pricing, capacity, underwriting, limits, deductibles and coverages.

-

Article 12 mins

Q4 2023: Global Insurance Market Overview -

Article 13 mins

Top Risk Trends to Watch in 2024

Regional Results

How do the top risks on business leaders’ minds differ by region and how can these risks be mitigated? Explore the regional results to learn more.

-

Article 12 mins

Top Risks Facing Organizations in Asia Pacific -

Article 12 mins

Top Risks Facing Organizations in North America -

Article 10 mins

Top Risks Facing Organizations in Europe -

Article 8 mins

Top Risks Facing Organizations in Latin America -

Article 8 mins

Top Risks Facing Organizations in the Middle East and Africa -

Article 9 mins

Top Risks Facing Organizations in the United Kingdom

Human Capital Analytics

Our Human Capital Analytics collection gives you access to the latest insights from Aon's human capital team. Contact us to learn how Aon’s analytics capabilities helps organizations make better workforce decisions.

-

Article 14 mins

How Technology Will Transform Employee Benefits in the Next Five Years -

Podcast 18 mins

On Aon Podcast: Technology Impacting the Future of Health and Benefits -

Article 8 mins

Integrating Workforce Data to Uncover Hidden Insights -

Article 9 mins

How Employers Can Use Data to Improve Their Health Plans -

Podcast 24 mins

On Aon’s Better Being Series: Measuring Wellbeing -

Article 11 mins

Designing Tomorrow: Personalizing EVP, Benefits and Total Rewards -

Article 9 mins

How to Balance Cost with Growth in a Shifting Talent Market -

Article 8 mins

How Companies are Mitigating Rising Medical Costs -

Article 10 mins

How Data and Analytics Can Optimize HR Programs

Insights for HR

Explore our hand-picked insights for human resources professionals.

-

Article 7 mins

COVID-19 has Permanently Changed the Way We Think About Wellbeing -

Article 7 mins

DE&I in Benefits Plans: A Global Perspective -

Article 10 mins

How Data and Analytics Can Optimize HR Programs -

Article 9 mins

Why HR Leaders Must Help Drive Cyber Security Agenda -

Article 7 mins

Case Study: The LPGA Unlocks Talent Potential with Data -

Article 11 mins

Navigating the New EU Directive on Pay Transparency -

Article 4 mins

How to Design Better Talent Assessment to Promote DE&I -

Article 6 mins

Training and Transforming Managers for the Future of Work -

Article 7 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions -

Article 14 mins

Building a Resilient Workforce That Steers Organizational Success | An Outlook Across Industries

Workforce

Our Workforce Collection provides access to the latest insights from Aon’s Human Capital team on topics ranging from health and benefits, retirement and talent practices. You can reach out to our team at any time to learn how we can help address emerging workforce challenges.

-

Report 14 mins

A Workforce in Transition Prepares to Meet a Host of Challenges -

Article 17 mins

3 Strategies to Improve Career Outcomes for Older Employees -

Article 7 mins

Companies Need a Global Benefits Identity in an Era of Cost Containment -

Article 8 mins

Driving Inclusion and Diversity with Employee Benefits -

Article 17 mins

Five Big Human Resources Trends to Watch in 2024 -

Article 8 mins

How Companies are Mitigating Rising Medical Costs -

Report 1 mins

The Global Medical Trend Rates Report 2025 -

Podcast 25 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience -

Article 9 mins

How the Right Employee Wellbeing Strategy Impacts Microstress and Burnout at Work -

Article 11 mins

Advancing Women’s Health and Equity Through Benefits and Support -

Podcast 18 mins

On Aon Podcast: Technology Impacting the Future of Health and Benefits -

Article 7 mins

How Collective Retirement Plans Help Support Financial Sustainability

Mergers and Acquisitions

Our Mergers and Acquisitions (M&A) collection gives you access to the latest insights from Aon's thought leaders to help dealmakers make better decisions. Explore our latest insights and reach out to the team at any time for assistance with transaction challenges and opportunities.

-

Article 8 mins

Exit Strategy Value Creation Opportunities Exist as Economic Pressures Persist -

Article 5 mins

Future Trends for Financial Sponsors: Secondary Transactions -

Article 7 mins

3 Ways to Unlock M&A Value in a Challenging Credit Environment -

Article 7 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions -

Article 9 mins

Organizational Design and Talent Planning are Key to M&A Success -

Article 7 mins

An Ever-Complex Global Tax Environment Requires Strong M&A Risk Solutions -

Article 6 mins

Project Management for HR: The Secret Behind a Successful M&A Deal -

Article 9 mins

Cultural Alignment Planning Drives M&A Success -

Report 1 mins

A Guide to Maximizing Value in Post-Merger Integrations -

Report 2 mins

The ABC's of Private Equity M&A: Deal Flow Impacts of Al, Big Tech and Climate Change -

Article 11 mins

The Silver Lining on M&A Deal Clouds: M&A Insurance Insights from 2023

Navigating Volatility

How do businesses navigate their way through new forms of volatility and make decisions that protect and grow their organizations?

Parametric Insurance

Our Parametric Insurance Collection provides ways your organization can benefit from this simple, straightforward and fast-paying risk transfer solution. Reach out to learn how we can help you make better decisions to manage your catastrophe exposures and near-term volatility.

-

Article 10 mins

How Public Entities and Businesses Can Use Parametric for Emergency Funding -

Article 6 mins

Parametric Insurance: A Complement to Traditional Property Coverage -

Article 8 mins

Using Parametric Insurance to Match Capital to Climate Risk -

Article 6 mins

Using Parametric Insurance to Close the Earthquake Protection Gap -

Article 5 mins

How Technology Enhancements are Boosting Parametric

Pay Transparency and Equity

Our Pay Transparency and Equity collection gives you access to the latest insights from Aon's human capital team on topics ranging from pay equity to diversity, equity and inclusion. Contact us to learn how we can help your organization address these issues.

-

Article 10 mins

How Financial Institutions can Prepare for Pay Transparency Legislation -

Article 8 mins

Pay Transparency Can Lead to Better Equity Across Benefits -

Article 12 mins

Understanding and Preparing for the Rise in Pay Transparency -

Podcast 14 mins

On Aon Podcast: Understanding Pay Transparency Regulations -

Article 11 mins

Navigating the New EU Directive on Pay Transparency -

Article 7 mins

To Disclose Pay or Not? How Companies are Approaching the Pay Transparency Movement -

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health -

Article 11 mins

Advancing Women’s Health and Equity Through Benefits and Support -

Article 8 mins

Driving Inclusion and Diversity with Employee Benefits -

Article 7 mins

Belonging at Work: How Employers can Strengthen DE&I -

Article 7 mins

DE&I in Benefits Plans: A Global Perspective -

Podcast 16 mins

On Aon Podcast: Approach to DE&I in the Workplace

Property Risk Management

Forecasters are predicting an extremely active 2024 Atlantic hurricane season. Take measures to build resilience to mitigate risk for hurricane-prone properties.

-

Article 8 mins

Florida Hurricanes Not Expected to Adversely Affect Property Market -

Article 10 mins

Build Resilience for an Extremely Active Atlantic Hurricane Season -

Article 6 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market -

Podcast 16 mins

On Aon Podcast: Navigating and Preparing for Catastrophes -

Article 6 mins

Parametric Insurance: A Complement to Traditional Property Coverage -

Article 6 mins

Navigating Climate Risk Using Multiple Models and Data Sets -

Article 5 mins

Rising Losses From Severe Convection Storms Mostly Explained by Exposure Growth -

Article 6 mins

Using Parametric Insurance to Close the Earthquake Protection Gap

Technology

Our Technology Collection provides access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities of technology. Reach out to the team to learn how we can help you use technology to make better decisions for the future.

-

Article 15 mins

How Artificial Intelligence is Transforming Human Resources and the Workforce -

Report 18 mins

Evolving Technologies Are Driving Firms to Harness Opportunities and Defend Against Threats -

Alert 3 mins

Better Decisions Brief: Perspectives on the CrowdStrike Outage -

Article 12 mins

5 Ways Artificial Intelligence can Boost Claims Management -

Article 6 mins

Artificial Intelligence and the Next Frontier for Financial Institutions -

Article 10 mins

Mitigating Insider Threats: Your Worst Cyber Threats Could be Coming from Inside -

Article 6 mins

8 Steps Toward Building Better Resilience Against Rising Ransomware Attacks -

Article 9 mins

Overcoming the Reputational Cost of Cyber Attacks: The 10-Day Plan -

Article 9 mins

Why HR Leaders Must Help Drive Cyber Security Agenda -

Article 5 mins

How Technology Enhancements are Boosting Parametric -

Article 9 mins

How to Futureproof Data and Analytics Capabilities for Reinsurers

Top 10 Global Risks

Trade, technology, weather and workforce stability are the central forces in today’s risk landscape.

-

Article 7 mins

Cyber Attack or Data Breach -

Article 4 mins

Business Interruption -

Article 4 mins

Economic Slowdown or Slow Recovery -

Article 5 mins

Failure to Attract or Retain Top Talent -

Article 5 mins

Regulatory or Legislative Changes -

Article 4 mins

Supply Chain or Distribution Failure -

Article 6 mins

Commodity Price Risk or Scarcity of Materials -

Article 4 mins

Damage to Brand or Reputation -

Article 5 mins

Failure to Innovate or Meet Customer Needs -

Article 4 mins

Increasing Competition -

Report 3 mins

Business Decision Maker Survey

Trade

Our Trade Collection gives you access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities for international business. Reach out to our team to understand how to make better decisions around macro trends and why they matter to businesses.

-

Article 8 mins

The Evolving Threat of Cargo Theft: 5 Key Mitigation Strategies -

Report 3 mins

Global Risk Management Survey -

Report 15 mins

Wide-Ranging Trade Issues Confront Global Businesses on Multiple Fronts -

Article 6 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market -

Article 14 mins

Cutting Supply Chains: How to Achieve More Reward with Less Risk -

Article 9 mins

Driving Private Equity Value Creation Through Credit Solutions -

Article 7 mins

4 Steps to Help Take Advantage of a Buyer-Friendly Directors' & Officers' Market -

Article 9 mins

Managing Reputational Risks in Global Supply Chains -

Article 6 mins

How an Outsourced Chief Investment Officer Can Help Improve Governance and Manage Complexity -

Article 8 mins

Decarbonizing Your Business: Finding the Right Insurance and Strategy -

Article 8 mins

Reputation Analytics as a Leading Indicator of ESG Risk

Weather

With a changing climate, organizations in all sectors will need to protect their people and physical assets, reduce their carbon footprint, and invest in new solutions to thrive. Our Weather Collection provides you with critical insights to be prepared.

-

Article 8 mins

Florida Hurricanes Not Expected to Adversely Affect Property Market -

Report 16 mins

Climate Analytics Unlock Capital to Protect People and Property -

Report 3 mins

Climate and Catastrophe Insight -

Article 10 mins

How Public Entities and Businesses Can Use Parametric for Emergency Funding -

Podcast 12 mins

On Aon Podcast: Tackling Climate Risk to Build Economic Resilience -

Article 8 mins

Understanding Freeze Risk in a Changing Climate -

Podcast 9 mins

On Aon Podcast: Climate Science Through Academic Collaboration -

Article 6 mins

How Companies Are Using Climate Modeling to Improve Risk Decisions -

Podcast 7 mins

On Aon Insights: Climate and Supply Chain -

Article 8 mins

Using Parametric Insurance to Match Capital to Climate Risk -

Article 9 mins

How the Construction Industry is Navigating Climate Change -

Article 9 mins

Record Heatwaves: Protecting Employee Health and Safety

Workforce Resilience

Our Workforce Resilience collection gives you access to the latest insights from Aon's Human Capital team. You can reach out to the team at any time for questions about how we can assess gaps and help build a more resilience workforce.

-

Article 7 mins

Using Data to Close Workforce Gaps in Financial Institutions -

Article 5 mins

Using Data to Close Workforce Gaps in Retail Companies -

Article 7 mins

Using Data to Close Workforce Gaps in Technology Companies -

Article 5 mins

Using Data to Close Workforce Gaps in Manufacturing Companies -

Article 6 mins

Using Data to Close Workforce Gaps in Life Sciences Companies -

Report 4 mins

Measure Workforce Resilience for Better Business Outcomes -

Podcast 18 mins

On Aon Podcast: Methodology to Predict Employee Performance for the LPGA -

Article 6 mins

Training and Transforming Managers for the Future of Work -

Article 14 mins

Building a Resilient Workforce That Steers Organizational Success | An Outlook Across Industries

More Like This

-

Article 6 mins

Leading the Biofuels Transition: Risk Strategies to Cut Through Complexity

Companies aiming to be a net-zero company may face many challenges during the biofuels transition. Read more on risk strategies to cut through complexity.

-

Article 6 mins

DC Pension Schemes: Improving Investment Returns

With DC schemes growing across Europe, many organizations are realizing the importance of ensuring strong performance from their investments. Here’s how asset owners and managers can optimize DC outcomes through the right investment strategy.

-

Article 9 mins

Developing a Paid Leave Strategy That Supports Workers and Their Families

With no federal paid leave law in the U.S., employers have limited guidance in designing equitable and comprehensive paid leave programs to support their workforce. Looking beyond compliance to focus on strategy and values will help create fair and well-designed policies.