Article

2023 can be best summarized with a single word: resilience.

Resilience amidst economic volatility fueled by spikes in interest rates and inflation. Resilience despite geopolitical instability, social unrest, and humanitarian crises spanning multiple continents. Resilience in the face of devastating natural disasters and mounting climate concerns. While every community, business, and economy has forged their own unique journey, resilience has been a common denominator.

Resilience shaped the risk and insurance community in 2023 as well. Economic inflation, a slow supply chain recovery, rising labor costs and persistent natural disaster activity pressured property loss costs and extended recovery periods. Social inflation, “nuclear verdicts”, and litigation funding drove up liability losses – especially related to U.S. exposures. New automotive technologies and distracted driving continued to alter the auto risk landscape. The regulatory environment became more complex and focused on addressing matters related to insurer solvency, cyber incident disclosures, and the use of generative Artificial Intelligence, amongst many other issues.

Over the course of the year, insurers responded to these and other dynamics of the risk and insurance environment by implementing their own resiliency measures, some of which impacted insurance market conditions. They undertook various measures, including refocusing their appetite, adjusting their underwriting policies, shifting their pricing models, streamlining their organizations, and aligning with business partners who share their values.

These market dynamics played out decidedly in the final quarter of 2023. We saw healthy appetite, underwriting flexibility, the availability of coverage options, and abundant capacity for well-performing, preferred risk types, as insurers sought to meet year-end performance targets. By contrast, challenging risk types and areas not targeted for insurer growth faced greater underwriting scrutiny, higher pricing and had fewer options. Across all risks, robust underwriting information and risk differentiation were key drivers of superior renewal outcomes, and evidence of investment in corporate responsibility initiatives continued to positively impact underwriting decisions.

Looking ahead, we expect many of the economic, geopolitical, and humanitarian events that shaped 2023 to continue to evolve in 2024, and new trends to emerge, creating challenges as well as opportunities. In this edition of Aon’s Global Insurance Market Insights report, we highlight five trends to watch in the short to medium term, including:

1. Cyber attackers will continue to exploit vulnerabilities and adapt their methods to sidestep controls, gain unauthorized access to systems, and exfiltrate information from corporate infrastructures. In addition, insider risk stemming from IT layoffs, companies’ use of AI and other emerging technologies, and an increase in class action and other civil and criminal lawsuits related to data protection and privacy will likely pose new challenges.

2. Core inflation will remain subject to volatility stemming from geopolitical instability and changes in economic policy. At the same time, the scourge of social inflation will likely continue unabated creating more volatility for corporations and an invisible tax on consumers.

3. Demand for parametric covers will continue to increase as organizations seek 1) quick liquidity after a disruptive event, 2) to address gaps in traditional insurance cover and 3) to cover non-traditional risks (non-damage business interruption, contingent exposures, and many more).

4. The worker-driven market will continue as unemployment rates remain at record lows, prompting employers to adapt their growth agendas to recognize the need for competitive benefits and accommodating work environments. Worker upskilling and reskilling will be prioritized in workforce planning strategies.

5. The energy transition will require significant investment in infrastructure, new technologies and process enhancements as demand for cleaner energy sources increases. Government policy – including subsidies and tax advantages – will serve as a key enabler of investments. Supply chains will be vulnerable to increased reliance on certain raw materials, new technologies and manufactured goods. Higher interest rates and inflation will create challenges to raise and deploy capital for investment in new assets.

Learn more about these complex, interconnected trends and their potential impacts on the risk and insurance environment in the 2024 Trends to Watch section of this report.

Article

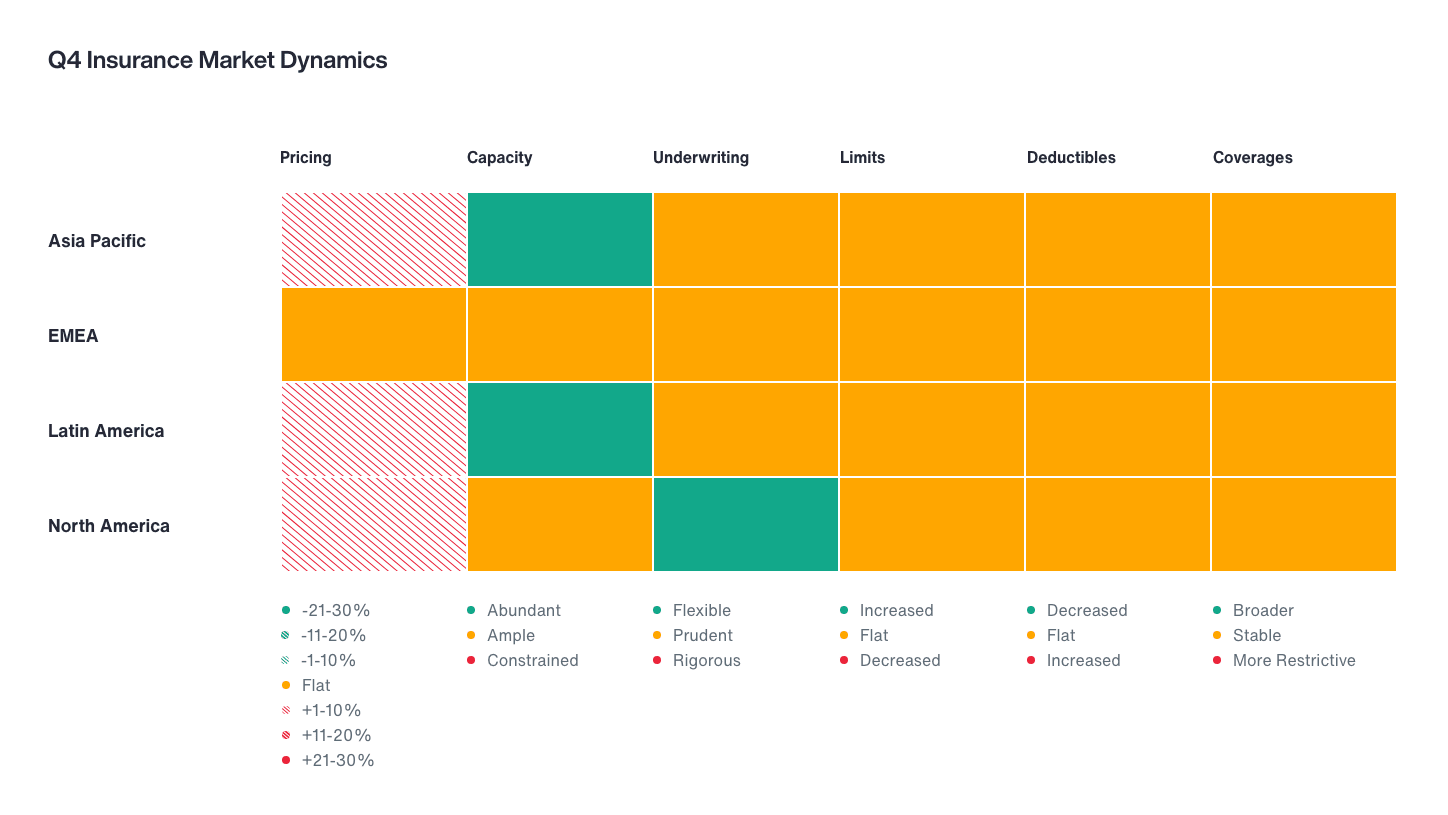

Expand the options below to read a summary of how the insurance market trended in Q4 2023 across pricing, capacity, underwriting, limits, deductibles and coverages.

Pricing was pressured by inflation but remained moderate. Challenged risk profiles and risks with adverse loss experience such as Natural Catastrophe-exposed Property risks and Liability risks with significant U.S exposures experienced more significant price increases.

As established insurers expanded their appetite and new insurers entered markets targeted for growth, well-performing risks experienced healthy competition and abundant capacity. Some risks with challenging profiles or adverse loss experience saw capacity limitations and many sought alternative risk transfer solutions.

While underwriting remained disciplined as respects valuations, risk quantification, and matters related to corporate responsibility, insurers’ year-end growth targets led to more flexibility and client options, particularly for preferred risk types. Robust underwriting information and risk differentiation supported superior renewal outcomes.

Expiring limits were available across most placements. Some insureds sought to reinvest their premium savings in increased limits. Increased limits were often available for well-performing risks and for products experiencing strong insurer appetite for growth (e.g., Cyber and Directors & Officers).

Expiring deductibles were achieved across most placements. Some insureds sought to reinvest their premium savings in deductible decreases. Such decreases were often available for well performing risks and for products experiencing strong insurer appetite for growth (e.g., Cyber and Directors & Officers).

Insurers continued to leverage coverage terms as a differentiator, and coverage enhancements, supported by quality underwriting information, remained available for some risks. Some restrictions (e.g., related to Communicable Disease, Coverage Territory, per-and polyfluoroalkyl substances (PFAS), and Strikes Riot and Civil Commotion) remained effectively non-negotiable.

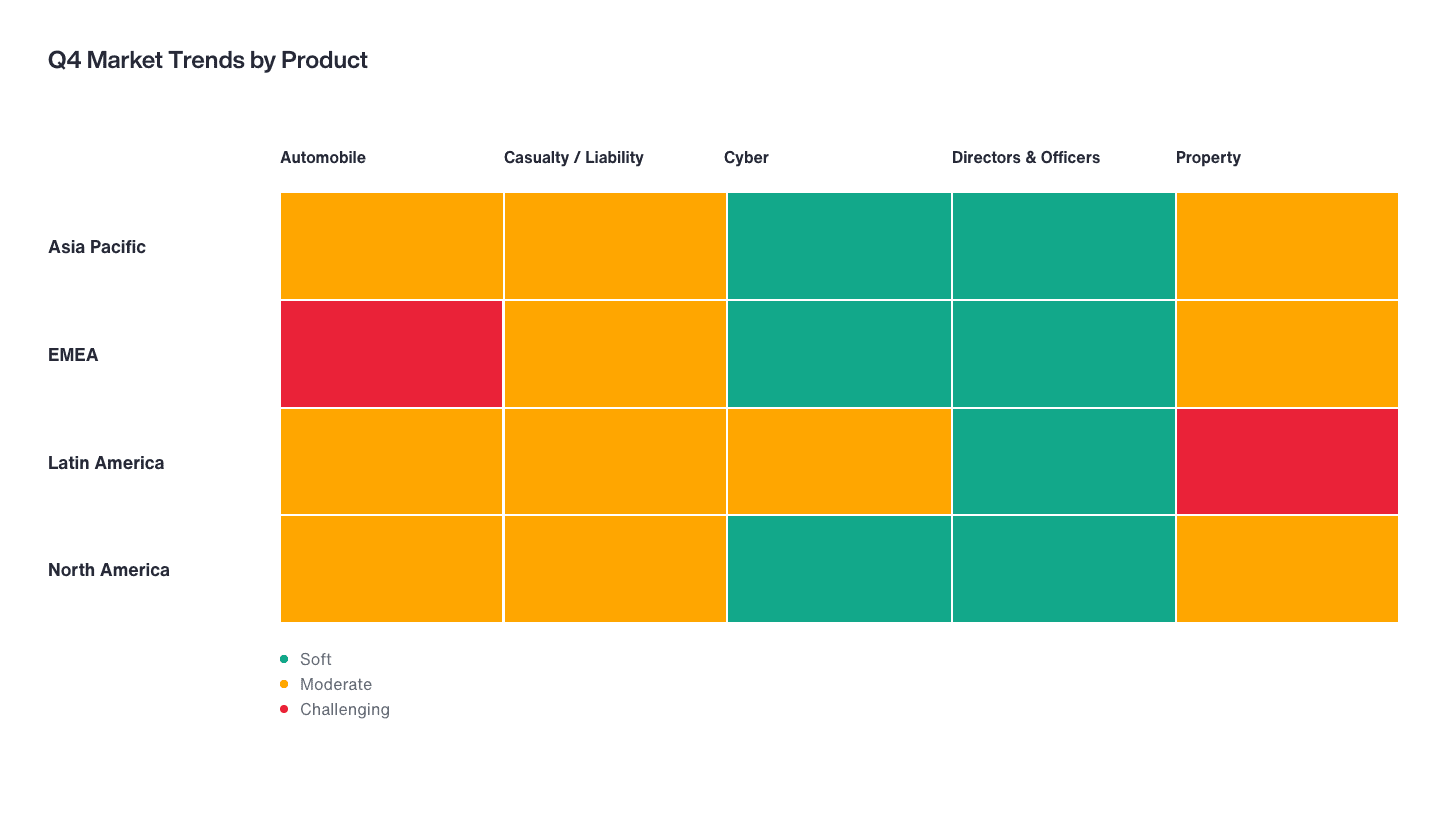

Expand the options below to read a summary of how the insurance market trended in Q4 2023 across key lines of business, including Automobile, Casualty/Liability, Cyber, Directors & Officers and Property.

Insurer appetite and capacity deployment was dampened by claims inflation stemming largely from higher parts and labor costs, increased accident frequency, ongoing supply chain disruptions, and increasing use of costly-to-repair automotive technologies. Underwriting remained disciplined and focused on risk management and overall portfolio sustainability. Risk differentiation, including the use of telematics and other vehicle safety and driver training initiatives, remained important.

Challenged risk profiles, risks with adverse loss experience, and Umbrella and Excess programs with lower Primary attachment points, experienced moderately challenging market conditions including rate increases, underwriting scrutiny, and capacity limitations. Well-performing, in-appetite risks experienced a more growth-focused environment, including some downward price movements. Social inflation and U.S. exposure – and the potential for “nuclear verdicts” – was a key underwriting consideration and cost driver. Underwriters became more conservative in their per-and polyfluoroalkyl substance (PFAS) mandates.

Despite ongoing cyber incidents, buyer friendly market conditions continued, with robust competition and abundant capacity as incumbent insurers sought to retain their renewals and potentially expand their participation, while newer entrants competed aggressively as they sought to develop their Cyber product. Underwriting requirements remained consistent, particularly related to cyber security and other risk management practices. Privacy-related losses remained a key insurer concern, with a specific focus on biometric data and pixel tracking, as well as emerging enforcement of privacy/consumer protection regulations. War and systemic risk also remained a top concern for insurers, and they continued to evaluate, scrutinize, and in some instances restrict coverage offered for critical infrastructure, systemic and/or correlated events, and war. Risk differentiation and evidence of best-in-class security / privacy controls were key to achieving superior renewal results.

Buyer-friendly market conditions continued, driven largely by abundant capacity from new and established insurers combined with a lack of new buyers (IPOs, deSPACs, etc.), as well as insurer focus on achieving year-end growth targets. Many insureds sought to reinvest their premium savings in deductible decreases, limit increases, and wording enhancements, which were available for some risks. Rising event-driven litigation and limit aggregation were key underwriting concerns.

Insurers sought profitable portfolio growth through pricing adequacy, targeted appetite, and disciplined underwriting. Modest-to-moderate rate increases continued for most risks while heavy industry and Natural Catastrophe-exposed or otherwise challenged risks, as well as Sabotage, Terrorism, and Political Violence coverages, experienced a more challenging pricing environment. Insurers remained focused on Natural Catastrophe capacity management; however, overall capacity remained generally sufficient as some insurers sought to expand their participation. Detailed underwriting information – including descriptions of valuation methodologies – and early engagement remained key to achieving superior renewal outcomes.

Expand the options below to read a summary of regional insurance market trends in Q4 2023. For the full details, download the PDF.

General Disclaimer

The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Terms of Use

The contents herein may not be reproduced, reused, reprinted or redistributed without the expressed written consent of Aon, unless otherwise authorized by Aon. To use information contained herein, please write to our team.

Our Better Being podcast series, hosted by Aon Chief Wellbeing Officer Rachel Fellowes, explores wellbeing strategies and resilience. This season we cover human sustainability, kindness in the workplace, how to measure wellbeing, managing grief and more.

Podcast 23 mins

Better Being Series: Understanding Burnout in the Workplace

Podcast 14 mins

Better Being Series: Why Nutrition Matters

Podcast 10 mins

Better Being Series: Discover the ‘Blue Zones’ Where People Live Longer

Podcast 20 mins

Better Being Series: Improving Your Financial Wellbeing

Podcast 17 mins

Better Being Series: Are You Taking Care of Your Digital Wellbeing?

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health

Podcast 29 mins

On Aon’s Better Being Series: The World Wellbeing Movement

Podcast 28 mins

On Aon’s Better Being Series: Mental Health and Creating Kinder Cultures

Podcast 25 mins

On Aon’s Better Being Series: Managing Loss and Grief

Podcast 24 mins

On Aon’s Better Being Series: Measuring Wellbeing

Podcast 25 mins

On Aon’s Better Being Series: Physical Wellbeing and Resilience

Podcast 24 mins

On Aon’s Better Being Series: Human SustainabilityExpert Views on Today's Risk Capital and Human Capital Issues

Article 8 mins

Thriving in an Interconnected World: How the C-Suite Embraces Uncertainty

Article 6 mins

Powering Progress: Collaborating to Build a Sustainable Future in Emerging Markets

Article 5 mins

Building Business Resilience: Key Steps to Effectively Integrate Risk Management Across Your Organisation

Article 7 mins

Why Humans Are the Essential Factor in the Success of Artificial Intelligence (AI)

Article 5 mins

Leveraging Research and Expertise to Strengthen Your HR Strategy for 2025 and Beyond

Article 5 mins

Managing Risk on the Energy Transition Journey

Article 7 mins

The Role of Risk Management in the Age of Generative Artificial Intelligence

Article 7 mins

Finding A Way In Asia Pacific's New Economic Reality

Article 4 mins

Three Ways to Boost Value from Benefits: APAC Insights from LinkedInExpert Views on Today's Risk Capital and Human Capital Issues

Expert Views on Today's Risk Capital and Human Capital Issues

Article 2 mins

Introduction: Clarity and Confidence to Make Better Decisions

Article 2 mins

The Age of Rising Resilience – An Economic Outlook

Article 3 mins

Building Resilience Against the Constant Cyber Threat

Article 2 mins

Making Better Decisions – A Treasurer’s Perspective

Article 2 mins

How to Balance the Conflicting Forces of Efficiency, Performance and Wellbeing

Article 3 mins

Seizing the Opportunity: Building a Comprehensive Approach to Risk Transfer

Article 2 mins

Tapping New Markets to Unlock Deal Value

Article 5 mins

The Rise of the Skills-Based Organisation

Article 2 mins

Creating a Fair and Equitable Workforce for Everyone

Article 3 mins

The Year of the Vote: How Geopolitical Volatility Will Impact Businesses

Article 2 mins

The Aon DifferenceThe construction industry is under pressure from interconnected risks and notable macroeconomic developments. Learn how your organization can benefit from construction insurance and risk management.

Article 8 mins

How North American Construction Contractors Can Mitigate Emerging Risks

Article 7 mins

Managing Construction Risks: 7 Risk Advisory Steps

Article 7 mins

Unlocking Capacity and Capital in a Challenging Construction Risk Market

Article 7 mins

Protecting North American Contractors from Extreme Heat Risks with Parametric

Article 5 mins

How Climate Modeling Can Mitigate Risks and Improve Resilience in the Construction Industry

Report 1 mins

Construction Risk Management Europe Report 2023

Article 8 mins

Parametric Can Help Mitigate Extreme Heat Risks for Contractors in EMEA

Article 9 mins

How the Construction Industry is Navigating Climate Change

Article 11 mins

Top Risks Facing Construction and Real Estate OrganizationsStay in the loop on today's most pressing cyber security matters.

Cyber Labs 17 mins

Maximizing value: How companies and pentesters can achieve more together

Cyber Labs 7 mins

DNSForge – Relaying with Force

Cyber Labs 14 mins

We’re All in This Together: The Case for Purple Teaming

Cyber Labs 7 mins

Parsing ESXi Logs for Incident Response with QELP

Cyber Labs 5 mins

Parsing Jenkins Configuration Files for Forensics and Fun

Cyber Labs 10 mins

Emerging Risks in Third-Party AI Solutions and How to Help Address Them

Cyber Labs 20 mins

Unveiling the Dark Side: Common Attacks and Vulnerabilities in Industrial Control Systems

Cyber Labs 9 mins

Mounted Guest EDR Bypass

Cyber Labs 6 mins

Optimizing Your Cyber Resilience Strategy Through CISO and CRO Connectivity

Cyber Labs 9 mins

Bypassing EDR through Retrosigned Drivers and System Time Manipulation

Cyber Labs 10 mins

DNSForge – Responding with Force

Cyber Labs 7 mins

Unveiling "sedexp": A Stealthy Linux Malware Exploiting udev Rules

Cyber Labs 3 mins

Command Injection and Path Traversal in StoneFly Storage Concentrator

Cyber Labs 7 mins

Adopt an AI Approach with Confidence, for CISOs and CIOs

Cyber Labs 3 mins

Responding to the CrowdStrike Outage: Implications for Cyber and Technology Professionals

Cyber Labs 10 mins

DUALITY Part II - Initial Access and Tradecraft Improvements

Cyber Labs 17 mins

Cracking Into Password Requirements

Cyber Labs 57 mins

DUALITY: Advanced Red Team Persistence through Self-Reinfecting DLL Backdoors for Unyielding Control

Cyber Labs 7 mins

Restricted Admin Mode – Circumventing MFA On RDP Logons

Cyber Labs 9 mins

Detecting “Effluence”, An Unauthenticated Confluence Web ShellOur Cyber Resilience collection gives you access to Aon’s latest insights on the evolving landscape of cyber threats and risk mitigation measures. Reach out to our experts to discuss how to make the right decisions to strengthen your organization’s cyber resilience.

Article 8 mins

Cyber and E&O Market Conditions Remain Favorable Amid Emerging Global Risks

Article 7 mins

How to Navigate AI-Driven Cyber Risks

Article 9 mins

Building Resilience in a Buyer-Friendly Cyber and E&O Market

Article 11 mins

A Middle Market Roadmap for Cyber Resilience

Article 7 mins

Lessons Learned from the CrowdStrike Outage: 5 Strategies to Build Cyber Resilience

Article 8 mins

Responding to Cyber Attacks: How Directors and Officers and Cyber Policies Differ

Article 7 mins

Why Now is the Right Time to Customize Cyber and E&O Contracts

Article 6 mins

8 Steps Toward Building Better Resilience Against Rising Ransomware Attacks

Article 7 mins

Mitigating Insider Threats: Managing Cyber Perils While Traveling Globally

Article 5 mins

Managing Cyber Risk through Return on Security Investment

Article 10 mins

Mitigating Insider Threats: Your Worst Cyber Threats Could be Coming from Inside

Article 9 mins

Why HR Leaders Must Help Drive Cyber Security Agenda

Article 10 mins

Escalating Cyber Security Risks Mean Businesses Need to Build ResilienceOur Employee Wellbeing collection gives you access to the latest insights from Aon's human capital team. You can also reach out to the team at any time for assistance with your employee wellbeing needs.

Article 8 mins

Employer Strategies for Cancer Prevention and Treatment

Article 6 mins

The Long-Term Care Conundrum in the United States

Article 9 mins

Developing a Paid Leave Strategy That Supports Workers and Their Families

Article 9 mins

4 Ways to Foster a Thriving Workforce Amid Rising Health Costs

Article 9 mins

The Next Evolution of Wellbeing is About Performance

Article 6 mins

Three Ways Collective Retirement Plans Support HR Priorities

Article 9 mins

How the Right Employee Wellbeing Strategy Impacts Microstress and Burnout at Work

Podcast 13 mins

On Aon Podcast: The Future of Healthcare: Key Factors Impacting Medical Trend Rates

Article 7 mins

Making Wellbeing Part of a Company’s DNA

Article 7 mins

A Comprehensive Approach to Financial WellbeingExplore Aon's latest environmental social and governance (ESG) insights.

Podcast 16 mins

On Aon Podcast: Approach to DE&I in the WorkplaceOur Global Insurance Market Insights highlight insurance market trends across pricing, capacity, underwriting, limits, deductibles and coverages.

Article 12 mins

Q4 2023: Global Insurance Market Overview

Article 13 mins

Top Risk Trends to Watch in 2024How do the top risks on business leaders’ minds differ by region and how can these risks be mitigated? Explore the regional results to learn more.

Article 12 mins

Top Risks Facing Organizations in Asia Pacific

Article 12 mins

Top Risks Facing Organizations in North America

Article 10 mins

Top Risks Facing Organizations in Europe

Article 8 mins

Top Risks Facing Organizations in Latin America

Article 8 mins

Top Risks Facing Organizations in the Middle East and Africa

Article 9 mins

Top Risks Facing Organizations in the United KingdomOur Human Capital Analytics collection gives you access to the latest insights from Aon's human capital team. Contact us to learn how Aon’s analytics capabilities helps organizations make better workforce decisions.

Article 35 mins

5 Human Resources Trends to Watch in 2025

Article 13 mins

Medical Rate Trends and Mitigation Strategies Across the Globe

Article 9 mins

3 Strategies to Help Avoid Workers Compensation Claims Litigation

Podcast 15 mins

On Aon Podcast: Using Data and Analytics to Improve Health Outcomes

Article 14 mins

How Technology Will Transform Employee Benefits in the Next Five Years

Podcast 18 mins

On Aon Podcast: Technology Impacting the Future of Health and Benefits

Article 8 mins

Integrating Workforce Data to Uncover Hidden Insights

Podcast 24 mins

On Aon’s Better Being Series: Measuring Wellbeing

Article 11 mins

Designing Tomorrow: Personalizing EVP, Benefits and Total RewardsExplore our hand-picked insights for human resources professionals.

Article 7 mins

COVID-19 has Permanently Changed the Way We Think About Wellbeing

Article 7 mins

DE&I in Benefits Plans: A Global Perspective

Article 10 mins

How Data and Analytics Can Optimize HR Programs

Article 9 mins

Why HR Leaders Must Help Drive Cyber Security Agenda

Article 7 mins

Case Study: The LPGA Unlocks Talent Potential with Data

Article 11 mins

Navigating the New EU Directive on Pay Transparency

Article 4 mins

How to Design Better Talent Assessment to Promote DE&I

Article 6 mins

Training and Transforming Managers for the Future of Work

Article 7 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions

Article 14 mins

Building a Resilient Workforce That Steers Organizational Success | An Outlook Across IndustriesOur Workforce Collection provides access to the latest insights from Aon’s Human Capital team on topics ranging from health and benefits, retirement and talent practices. You can reach out to our team at any time to learn how we can help address emerging workforce challenges.

Article 35 mins

5 Human Resources Trends to Watch in 2025

Article 19 mins

3 Strategies to Promote an Inclusive Environment and Bridge the Gender Gap

Report 13 mins

A Workforce in Transition Prepares to Meet a Host of Challenges

Article 8 mins

2025 Salary Increase Planning Tips

Article 8 mins

Employer Strategies for Cancer Prevention and Treatment

Article 12 mins

Understanding and Preparing for the Rise in Pay Transparency

Podcast 12 mins

Better Being Series: Building Sustainable Performance in a Multi-Generational Workforce

Article 7 mins

Key Trends in U.S. Benefits for 2025 and Beyond

Article 8 mins

Pay Transparency Can Lead to Better Equity Across Benefits

Article 17 mins

3 Strategies to Improve Career Outcomes for Older Employees

Article 9 mins

Developing a Paid Leave Strategy That Supports Workers and Their Families

Article 9 mins

4 Ways to Foster a Thriving Workforce Amid Rising Health CostsOur Mergers and Acquisitions (M&A) collection gives you access to the latest insights from Aon's thought leaders to help dealmakers make better decisions. Explore our latest insights and reach out to the team at any time for assistance with transaction challenges and opportunities.

Article 8 mins

Exit Strategy Value Creation Opportunities Exist as Economic Pressures Persist

Article 5 mins

Future Trends for Financial Sponsors: Secondary Transactions

Article 7 mins

3 Ways to Unlock M&A Value in a Challenging Credit Environment

Article 7 mins

Rethinking Your Total Rewards Programs During Mergers and Acquisitions

Article 9 mins

Organizational Design and Talent Planning are Key to M&A Success

Article 7 mins

An Ever-Complex Global Tax Environment Requires Strong M&A Risk Solutions

Article 6 mins

Project Management for HR: The Secret Behind a Successful M&A Deal

Article 9 mins

Cultural Alignment Planning Drives M&A Success

Report 1 mins

A Guide to Maximizing Value in Post-Merger Integrations

Report 2 mins

The ABC's of Private Equity M&A: Deal Flow Impacts of Al, Big Tech and Climate Change

Article 11 mins

The Silver Lining on M&A Deal Clouds: M&A Insurance Insights from 2023How do businesses navigate their way through new forms of volatility and make decisions that protect and grow their organizations?

Our Parametric Insurance Collection provides ways your organization can benefit from this simple, straightforward and fast-paying risk transfer solution. Reach out to learn how we can help you make better decisions to manage your catastrophe exposures and near-term volatility.

Article 10 mins

How Public Entities and Businesses Can Use Parametric for Emergency Funding

Article 6 mins

Parametric Insurance: A Complement to Traditional Property Coverage

Article 8 mins

Using Parametric Insurance to Match Capital to Climate Risk

Article 6 mins

Using Parametric Insurance to Close the Earthquake Protection Gap

Article 5 mins

How Technology Enhancements are Boosting ParametricOur Pay Transparency and Equity collection gives you access to the latest insights from Aon's human capital team on topics ranging from pay equity to diversity, equity and inclusion. Contact us to learn how we can help your organization address these issues.

Article 19 mins

3 Strategies to Promote an Inclusive Environment and Bridge the Gender Gap

Report 1 mins

The 2024 North America Pay Transparency Readiness Study

Article 10 mins

How Financial Institutions can Prepare for Pay Transparency Legislation

Article 8 mins

Pay Transparency Can Lead to Better Equity Across Benefits

Article 12 mins

Understanding and Preparing for the Rise in Pay Transparency

Podcast 14 mins

On Aon Podcast: Understanding Pay Transparency Regulations

Article 11 mins

Navigating the New EU Directive on Pay Transparency

Article 7 mins

To Disclose Pay or Not? How Companies are Approaching the Pay Transparency Movement

Podcast 19 mins

On Aon Podcast: Better Being Series Dives into Women’s Health

Article 11 mins

Advancing Women’s Health and Equity Through Benefits and SupportForecasters are predicting an extremely active 2024 Atlantic hurricane season. Take measures to build resilience to mitigate risk for hurricane-prone properties.

Article 8 mins

Florida Hurricanes Not Expected to Adversely Affect Property Market

Article 10 mins

Build Resilience for an Extremely Active Atlantic Hurricane Season

Article 6 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market

Podcast 16 mins

On Aon Podcast: Navigating and Preparing for Catastrophes

Article 6 mins

Parametric Insurance: A Complement to Traditional Property Coverage

Article 6 mins

Navigating Climate Risk Using Multiple Models and Data Sets

Article 5 mins

Rising Losses From Severe Convection Storms Mostly Explained by Exposure Growth

Article 6 mins

Using Parametric Insurance to Close the Earthquake Protection GapOur Technology Collection provides access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities of technology. Reach out to the team to learn how we can help you use technology to make better decisions for the future.

Article 23 mins

The AI Data Center Boom: Strategies for Sustainable Growth and Risk Management

Article 7 mins

How Technology is Transforming Open Enrollment in the U.S.

Article 15 mins

Navigating Cyber Risks in EMEA: Key Insights for 2025

Article 7 mins

How to Navigate AI-Driven Cyber Risks

Article 16 mins

How Artificial Intelligence is Transforming Human Resources and the Workforce

Report 18 mins

Evolving Technologies Are Driving Firms to Harness Opportunities and Defend Against Threats

Alert 3 mins

Better Decisions Brief: Perspectives on the CrowdStrike Outage

Podcast 9 mins

On Aon Podcast: How has CrowdStrike Changed the Cyber Market?

Article 12 mins

5 Ways Artificial Intelligence can Boost Claims Management

Article 12 mins

Navigating AI-Related Risks: A Guide for Directors and Officers

Article 5 mins

How Technology Enhancements are Boosting Parametric

Article 9 mins

How to Futureproof Data and Analytics Capabilities for ReinsurersTrade, technology, weather and workforce stability are the central forces in today’s risk landscape.

Article 7 mins

Cyber Attack or Data Breach

Article 4 mins

Business Interruption

Article 4 mins

Economic Slowdown or Slow Recovery

Article 5 mins

Failure to Attract or Retain Top Talent

Article 5 mins

Regulatory or Legislative Changes

Article 4 mins

Supply Chain or Distribution Failure

Article 6 mins

Commodity Price Risk or Scarcity of Materials

Article 4 mins

Damage to Brand or Reputation

Article 5 mins

Failure to Innovate or Meet Customer Needs

Article 4 mins

Increasing Competition

Report 3 mins

Business Decision Maker SurveyOur Trade Collection gives you access to the latest insights from Aon's thought leaders on navigating the evolving risks and opportunities for international business. Reach out to our team to understand how to make better decisions around macro trends and why they matter to businesses.

Podcast 9 mins

Special Edition: Global Trade and its Impact on Supply Chain

Article 8 mins

The Evolving Threat of Cargo Theft: 5 Key Mitigation Strategies

Report 3 mins

Global Risk Management Survey

Report 13 mins

Wide-Ranging Trade Issues Confront Global Businesses on Multiple Fronts

Article 6 mins

Four Steps to Develop Strong Property Risk Coverage in a Hardening Market

Article 14 mins

Cutting Supply Chains: How to Achieve More Reward with Less Risk

Article 9 mins

Driving Private Equity Value Creation Through Credit Solutions

Article 7 mins

4 Steps to Help Take Advantage of a Buyer-Friendly Directors' & Officers' Market

Article 9 mins

Managing Reputational Risks in Global Supply Chains

Article 6 mins

How an Outsourced Chief Investment Officer Can Help Improve Governance and Manage Complexity

Article 8 mins

Decarbonizing Your Business: Finding the Right Insurance and Strategy

Article 8 mins

Reputation Analytics as a Leading Indicator of ESG RiskWith a changing climate, organizations in all sectors will need to protect their people and physical assets, reduce their carbon footprint, and invest in new solutions to thrive. Our Weather Collection provides you with critical insights to be prepared.

Podcast 9 mins

On Aon Podcast: Climate Impact on the Property and Casualty Market

Alert 14 mins

L.A. Wildfires Highlight Urgent Need for Employee Support and Business Resilience

Report 18 mins

Climate Analytics Unlock Capital to Protect People and Property

Report 2 mins

Climate and Catastrophe Insight

Article 10 mins

How Public Entities and Businesses Can Use Parametric for Emergency Funding

Podcast 12 mins

On Aon Podcast: Tackling Climate Risk to Build Economic Resilience

Article 8 mins

Understanding Freeze Risk in a Changing Climate

Podcast 9 mins

On Aon Podcast: Climate Science Through Academic Collaboration

Article 6 mins

How Companies Are Using Climate Modeling to Improve Risk Decisions

Article 8 mins

Using Parametric Insurance to Match Capital to Climate Risk

Article 9 mins

How the Construction Industry is Navigating Climate Change

Article 9 mins

Record Heatwaves: Protecting Employee Health and SafetyOur Workforce Resilience collection gives you access to the latest insights from Aon's Human Capital team. You can reach out to the team at any time for questions about how we can assess gaps and help build a more resilience workforce.

Article 4 mins

Using Data to Close Workforce Gaps in Financial Institutions

Article 5 mins

Using Data to Close Workforce Gaps in Retail Companies

Article 7 mins

Using Data to Close Workforce Gaps in Technology Companies

Article 5 mins

Using Data to Close Workforce Gaps in Manufacturing Companies

Article 6 mins

Using Data to Close Workforce Gaps in Life Sciences Companies

Report 4 mins

Measure Workforce Resilience for Better Business Outcomes

Podcast 18 mins

On Aon Podcast: Methodology to Predict Employee Performance for the LPGA

Article 6 mins

Training and Transforming Managers for the Future of Work

Article 14 mins

Building a Resilient Workforce That Steers Organizational Success | An Outlook Across Industries

Article

To be successful, business leaders must keep pace with the key trends that will impact the risk and insurance landscape in 2024.

Article

Generative Artificial Intelligence (AI) – a type of artificial intelligence that has the ability to create material such as images, music or text – is already a proven disruptor and its adoption is growing at an explosive rate.

Report

This quarter’s report describes some of the important developments in the Q4 insurance market and includes special features (on topics such as Generative AI and “Nuclear Verdicts”) to help you navigate the complexities and challenges of today’s risk and insurance environment.

You will soon receive an email to verify your email address. Please click on the link included in this note to complete the subscription process, which also includes providing consent in applicable locations and an opportunity to manage your email preferences.

Article 5 Min Read

Article 10 Min Read

Your request is being reviewed so we can align you to the best resources on our team. In the meantime, we invite you to explore some of our latest insights below.

Article 5 Min Read

Article 10 Min Read