Why Parametric Solutions Should Be Part of Your Next Renewal Conversation

Why Parametric Solutions Should Be Part of Your Next Renewal Conversation

October 6, 2023 8 mins

Why Parametric Solutions Should Be Part of Your Next Renewal Conversation

With continued market volatility, finding adequate coverage for growing protection gaps via traditional insurance alone is challenging. Parametric solutions can help businesses build resiliency against catastrophe-prone exposures and more.

Key Takeaways

Risk managers are increasingly deploying ART solutions such as parametric to fill protection gaps and take better control of their risks.

Parametric insurance has become an important strategic tool to mitigate natural catastrophes and other risks in a hard property market.

Parametric products are independent, fast and flexible event-based versus loss-based solutions that enable access to coverage under any market condition.

As capacity shrinks and rates increase in the traditional property insurance market, risk managers are creatively rethinking their risk resilience strategies.

There are a variety of alternative risk transfer (ART) solutions that risk buyers are using to address growing protection gaps, while also adding flexibility into their renewal decisions.

Parametric insurance has emerged as a compelling and unique option, especially in catastrophe-prone areas. It provides a different way to think about mitigating risk, especially if conventional products are restricted, unavailable or not meeting an organization's needs.

Building A Resilient Business with Parametric Solutions

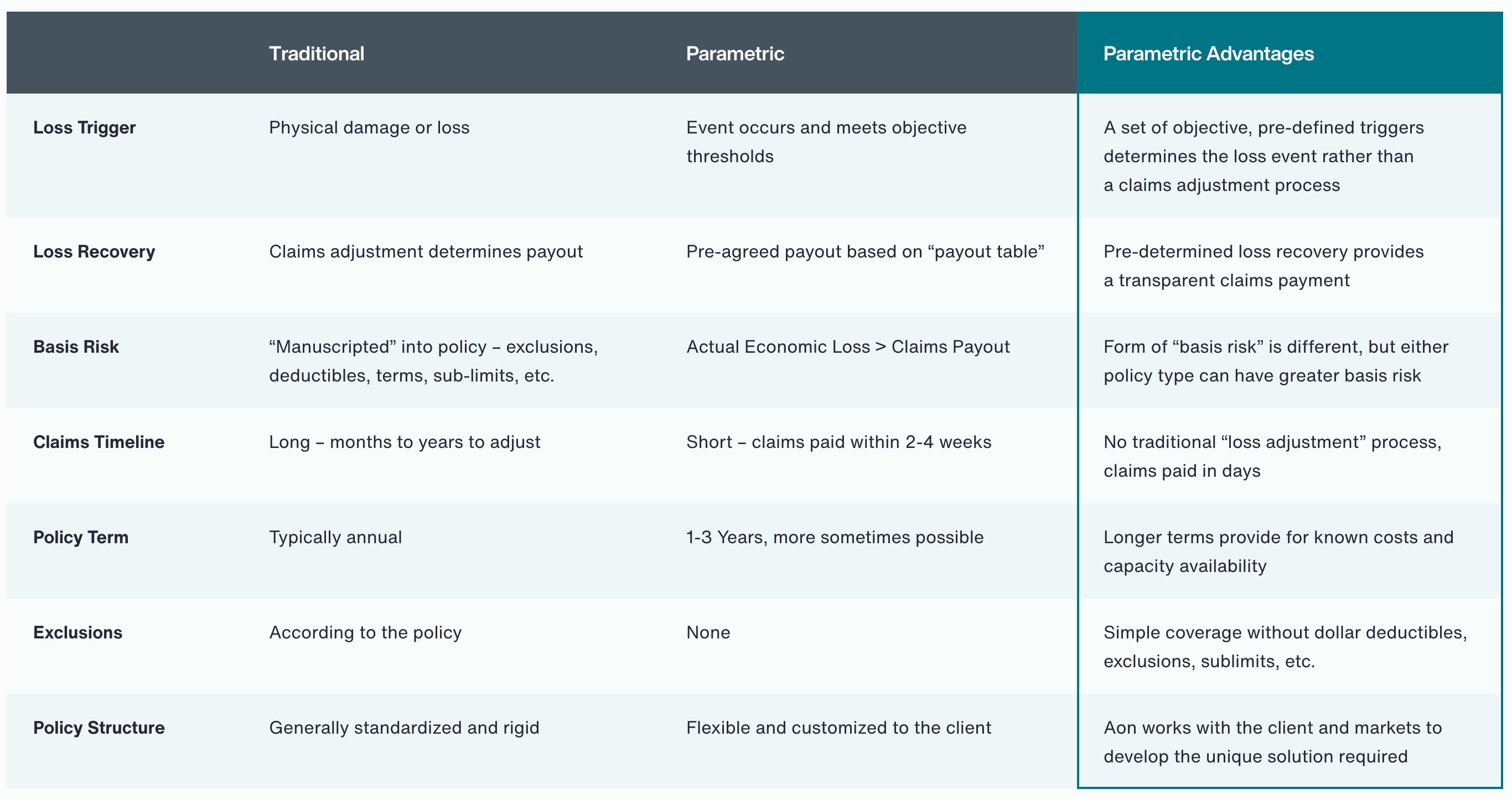

Parametric coverage is triggered when predefined parameter thresholds measured and reported by a third party are met. As a result, what was once considered uninsurable is now insurable. Claims payments are also made within weeks, freeing up capital when a business most needs it.

“Parametric insurance has a two-pronged value proposition as compared to traditional insurance,” says Michael Gruetzmacher, Aon’s head of Alternative Risk Transfer and Innovation.

“First, it transforms how insurance works through an alternative claims process that results in faster payouts, making it a liquidity instrument. Second, it transforms coverage to a ‘brute-force’ approach that covers any economic loss from a trigger event vs. the ‘surgical’ approach of traditional insurance, which typically results in protection gaps.”

In catastrophe-prone areas where market capacity is limited and rates continue to rise, for example, parametric insurance has become an important strategic tool. It allows risk managers to take better control of their risks with an “if-then” model that complements and supplements existing indemnity programs.

“One of the advantages of parametric insurance is that it allows carriers to price things directly,” says Peter Lacovara, managing director of Aon’s Alternative Risk Transfer and Innovation.

“The same carriers might be more willing to deploy parametric limits over conventional ones because they have a very clear understanding of how the policy is priced and how they could potentially lose money,” he adds. “With conventional indemnity, there are all kinds of nuances involved.”

Three Reasons to Implement a Pro-Parametric Renewal Strategy

1. Speed of Payment: Because the index value from a third-party trigger can be verified quickly, a claim can be paid within days after an event. This allows for fast post-event liquidity to deal with the immediate aftermath of a disruptive event.

2. Broadness of Cover: Payment can be used for any resulting financial loss from an event, with no deductible applied. Further expenses and losses that are typically excluded under a traditional indemnity policy can be addressed.

3. Flexibility in Design: Parametric can be customized to solve for specific coverage issues that may be difficult for traditional insurance. This could include supply chain, non-damage business interruption, loss of attraction, loss of ingress/egress and sub-limited or excluded coverages.

“By working with qualified industry leaders and third-party data providers on risk events, businesses can quantify their exposure by location and create customized parametric triggers to accelerate recovery from hard-to-estimate economic losses,” says Kirstin McMullan, Aon’s Principal Consultant for Natural Catastrophe in Australia.

Managing Future Risk With Parametric Solutions

Parametric products are independent, fast and flexible solutions that enable businesses to access coverage under any market condition. They can be leveraged with traditional methods as an additional avenue of recourse for typically uninsured events, while also serving as a supplementary protection gap filler for navigating the volatility of future markets.

Many exogenous, non-damage business interruption events, such as COVID-19, are not readily addressed by existing insurance solutions. As the industry collectively works to enhance resiliency for these kinds of events and other emerging risks, parametric insurance can be a key tool to match capital to risk and make better risk decisions.

Parametric Insurance Addresses Many Diverse Business Needs

Hedges traditional insurance both in time (settles quickly while traditional is being adjusted) and in coverage (broad coverage fills in the gaps within a traditional insurance policy).

Can provide supplemental capacity when programs are difficult to fill.

Difficult-to-Insure or Uninsurable Risk

Parametric can cover risks that the traditional market struggles to address.

Some examples include transmission and distribution lines, solar assets, hazardous or exposed occupancies, older structures, etc.

Non-Damage Business Interruption

Due to the broad definition of loss (wherein physical damage at the client’s assets is not required), parametric covers can address financial loss that the client incurs as a result of wide area damage or infrastructure disruption.

This would include various types of contingent business interruption loss resulting from damage to key suppliers or customers.

New Exposures

Parametric insurance can cover exposures not previously considered insurable under any traditional policy.

A few examples include employee assistance following a major event and public entity’s loss of tax revenue.

Parametric insurance can be seen as the catalyst for the future. It unlocks new solutions and access to capital through the straightforward nature of its underwriting process and the simplicity of the product itself.

Michael Gruetzmacher

Head of Alternative Risk Transfer and Innovation, North America

Aon's Thought Leaders

Michael Gruetzmacher

Head of Alternative Risk Transfer and Innovation, North America

Peter Lacovara

Managing Director, Alternative Risk Transfer and Innovation, North America

Kirstin McMullan

Principal Consultant, Natural Catastrophe, Australia

Tracy Riddell

Head, Placement, Property & Casualty, Australia

Sam Ketley

Head, Enterprise Risk Solutions, New Zealand

General Disclaimer

This document is not intended to address any specific situation or to provide legal, regulatory, financial, or other advice. While care has been taken in the production of this document, Aon does not warrant, represent or guarantee the accuracy, adequacy, completeness or fitness for any purpose of the document or any part of it and can accept no liability for any loss incurred in any way by any person who may rely on it. Any recipient shall be responsible for the use to which it puts this document. This document has been compiled using information available to us up to its date of publication and is subject to any qualifications made in the document.

Terms of Use

The contents herein may not be reproduced, reused, reprinted or redistributed without the expressed written consent of Aon, unless otherwise authorized by Aon. To use information contained herein, please write to our team.

Aon's Better Being Podcast

Our Better Being podcast series, hosted by Aon Chief Wellbeing Officer Rachel Fellowes, explores wellbeing strategies and resilience. This season we cover human sustainability, kindness in the workplace, how to measure wellbeing, managing grief and more.

The construction industry is under pressure from interconnected risks and notable macroeconomic developments.

Learn how your organization can benefit from construction insurance and risk management.

Our Cyber Resilience collection gives you access to Aon’s latest insights on the evolving landscape of cyber threats and risk mitigation measures. Reach out to our experts to discuss how to make the right decisions to strengthen your organization’s cyber resilience.

Our Employee Wellbeing collection gives you access to the latest insights from Aon's human capital team. You can also reach out to the team at any time for assistance with your employee wellbeing needs.

Our Human Capital Analytics collection gives you access to the latest insights from Aon's human capital team. Contact us to learn how Aon’s analytics capabilities helps organizations make better workforce decisions.

Our Workforce Collection provides access to the latest insights from Aon’s Human Capital team on topics ranging from health and benefits, retirement and talent practices. You can reach out to our team at any time to learn how we can help address emerging workforce challenges.